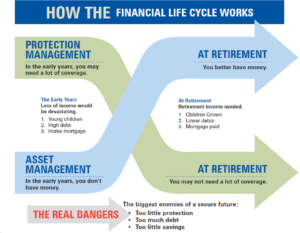

Understanding the Financial Life Cycle: Essential for Every Stage

Here’s a basic overview of how life insurance needs typically evolve over the course of an individual’s or a young family’s Financial Life Cycle:

- Young and Single: At this stage, an individual might have minimal financial obligations, and the need for life insurance is typically low. However, even at this stage, there might be a need for a small policy to cover final expenses or debts.

- Married Without Children: When a person marries, there could be combined debts, a mortgage, or the financial well-being of a spouse to consider. While the need for life insurance increases, it’s still relatively moderate compared to later stages.

- Young Families: This is when life insurance becomes particularly crucial. With young children dependent on parents’ income, significant debts (like mortgages), and other financial responsibilities, the death of a breadwinner can be financially devastating. Therefore, life insurance needs are at their peak during this period to ensure that the surviving family members are protected.

- Mature Families: As children grow older and become financially independent, and as significant debts (like mortgages) are paid down or off, the need for life insurance decreases. However, there might still be a need to protect against the loss of income, especially if one spouse has been out of the workforce for a long time.

- Pre-Retirement: At this stage, with most financial obligations met and perhaps with significant savings built up, the need for life insurance diminishes. Some might maintain policies to leave a legacy, cover potential estate taxes, or provide a financial cushion for a surviving spouse.

- Retirement: At retirement, the need for life insurance is usually at its lowest. Many financial obligations have been met, children are financially independent, and there might be retirement savings to rely on. However, some retirees might keep life insurance policies for specific reasons, such as leaving a legacy, covering final expenses, or helping with potential estate taxes.

It’s essential to note that everyone’s financial journey is unique, and insurance needs can vary based on specific circumstances, goals, and unforeseen life events. Regular reviews with a financial planner or insurance professional can help ensure that one’s coverage aligns with their current life stage and financial obligations.